Highlights

|

· |

Strategic plan remains on track and monthly breakeven expected during Q1 20231. The liability-led strategy and accelerated asset mix shift has successfully widened margins, further supported by the rising rate environment. |

|

· |

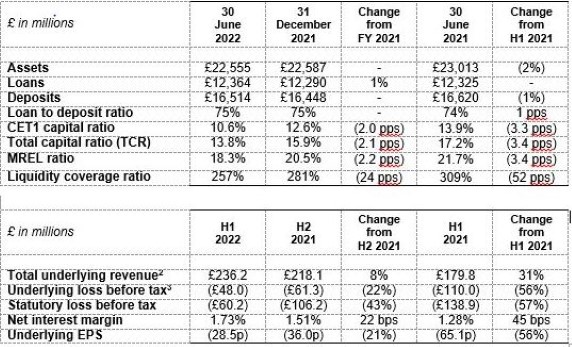

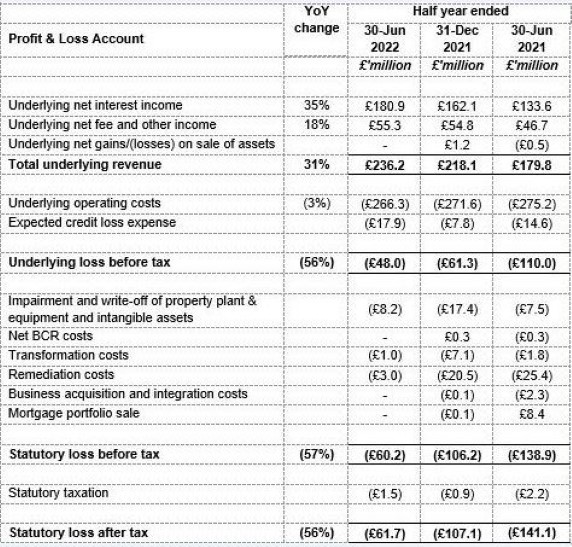

Total underlying revenue grew 31% YoY to £236.2 million (H1 2021: £179.8 million), demonstrating margin expansion and continued momentum in revenue growth as lending is optimised for return on regulatory capital. |

|

· |

Total underlying operating expenses fell 3% YoY to £266.3 million (H1 2021: £275.2 million) reflecting cost actions taken to reduce run-rate in the near term and limit future cost growth. |

|

· |

Cost of deposits reduced 17bps YoY to 0.14% (H1 2021: 0.31%) with the impact of rate rises offset by the continued focus on mix improvement, 47% of deposits are current accounts (H1 2021: 41%). |

|

· |

Underlying loss before tax of £48.0 million (H1 2021: loss of £110.0 million) reflects the significant growth in revenue and actions taken to reduce cost, offset marginally by increased expected credit loss provisions. |

|

· |

Statutory loss before tax of £60.2 million (H1 2021: loss of £138.9 million) includes one off items relating to capital neutral intangible asset write downs and remediation costs. Remediation costs of £3.0m (H1 2021: £25.4m) have reduced significantly as programs successfully conclude. |

|

· |

Announced appointment of James Hopkinson as CFO. |

- Assuming no material deterioration in the macro-economic environment.

Daniel Frumkin, Chief Executive Officer at Metro Bank, said:

“We have delivered a strong first-half performance and I am encouraged by the continued momentum we are seeing across the bank. Initiatives we have put in place have helped us to improve NIM and lending yield, and drive record revenue growth. We have also maintained our cost discipline and improved our cost to income ratio, with the focus on generating greater earnings from our capital base. As a result, we have built a sustainable business and we now expect to reach monthly breakeven during Q1 2023.

“All of this has been made possible by focusing on our turnaround strategy over the past two years. We also retain, at our core, fantastic colleagues delivering highly-rated customer service and we remain committed to being the UK’s best community bank. Collectively, we remain resolutely focused on continuing to execute our strategy and supporting our customers in the face of an increasingly complex macroeconomic environment.”

Key Financials:

- Underlying revenue excludes grant income recognised relating to the Capability & Innovation fund.

- Underlying loss before tax is an alternative performance measure and excludes impairment and write-off of property, plant & equipment (PPE) and intangible assets, net Banking Competition Remedies Limited (BCR) costs, transformation costs, remediation costs, business acquisition and integration costs and net income resulting from the mortgage portfolio sale when comparing to our statutory loss.

Financial performance for the half year ended 30 June 2022

Deposits

|

· |

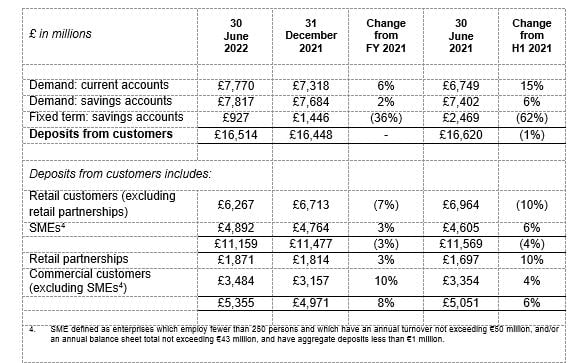

Total deposits held broadly flat in the first six months at £16,514 million as at 30 June 2022 (31 December 2021: £16,448 million), focus remained on mix improvement as current accounts increased by £452 million and fixed term deposit (FTD) accounts fell by £519 million. |

|

· |

Cost of deposits was 14bps in the first half, a decrease of 3bps compared to 17bps in H2 2021 despite the rising rate environment, the reduction continues to reflect the managed roll-off of higher cost FTD accounts and focus on mix improvement in favour of non-interest-bearing current accounts and demand savings accounts. |

|

· |

Customer account growth of 0.1 million (H2 2021: 0.1 million) in the last six months to 2.6 million, reflects stable growth in account openings and incremental growth from the RateSetter acquisition offset by the roll-off of FTDs. |

Loans

|

· |

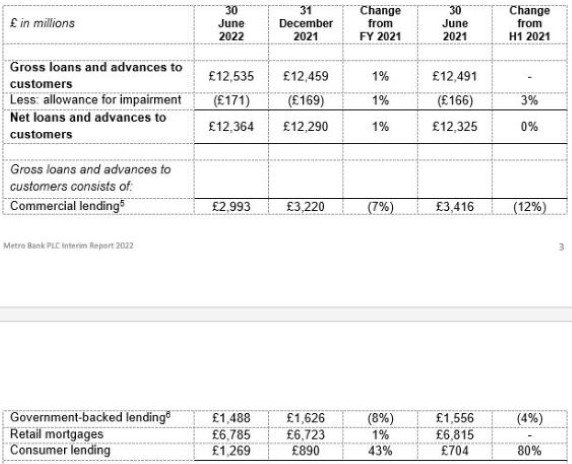

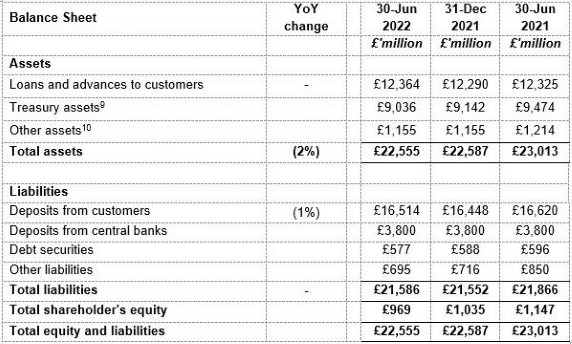

Total net loans as at 30 June 2022 were £12,364 million, broadly flat from £12,290 million at 31 December 2021 reflecting continued growth in consumer lending and specialist mortgages, offset by the attrition of lower-yielding residential mortgages and commercial term loans including commercial real estate. Total net loans are expected to increase in the second half of the year, with continuing mix shift towards higher yielding assets. |

|

· |

Commercial loans including commercial real estate (excluding BBLS, CBILS and RLS) decreased by 7% during H1 to £2,993 million at 30 June 2022 and are 12% below a year earlier following the attrition of lower-yielding commercial and commercial real estate term loans that provide a lower return on regulatory capital. |

|

· |

Retail mortgages remained the largest component of the lending book at 54%, with lower-yielding residential mortgages rolling off and focus shifting to specialist mortgages as part of the balance sheet optimisation strategy. Mortgage application volumes in Q2 2022 were 87% higher than Q1 and 133% higher than Q4 2021. |

|

· |

Consumer lending increased to 10% of the loan book from 7% at 31 December 2021, resulting from continued growth across all channels. Consumer originations averaged £105 million per month during H1 2022 and this trajectory is expected to continue. An approval rate of less than a third (29%) during the period shows the focus on selective credit quality. |

|

· |

Loan to deposit ratio remained stable at 75% (31 December 2021: 75%) reflecting the mix improvements in deposits and actions taken to optimise the balance sheet for accretive new lending despite current capital constraints. |

|

· |

Government-backed lending decreased 8% in the first half to £1,488 million at 30 June 2022 and is down 4% from a year earlier. |

|

· |

Annualised cost of risk at 0.29% (2H 2021: 0.12%) included recognition of ECL expense associated with organic growth in consumer lending. Non-performing loans reduced to 2.76% (31 December 2021: 3.71%) reflecting an improvement in Commercial single name exposures. The loan portfolio remains highly collateralised with average debt to value (DTV) of the residential mortgage book at 56% (31 December 2021: 55%), while DTV in the commercial book was 55% (31 December 2021: 57%). |

Profit and Loss Account

|

· |

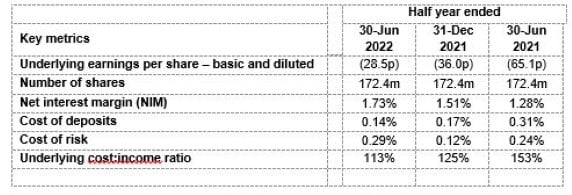

Net interest margin (NIM) at 1.73% has increased 22 bps in the first half, reflecting the impact of lower cost of deposits, improved lending mix and higher lending yields. |

|

· |

Underlying net interest income increased 12% in H1 2022 to £180.9 million (H2 2021: £162.1 million), and increased 35% YoY, highlighting the strong momentum in revenue following improvements in lending mix and the impact of rate rises. |

|

· |

Underlying net fee and other income increased 1% sequentially to £55.3 million (H2 2021: £54.8 million) driven by growth in Safe Deposit Boxes, Services Charges and Interchange partially offset by a reduction in FX, gains and other. Fees are expected to continue recovering. |

|

· |

Underlying cost: income ratio reduced to 113% in the first half of 2022, from 125% in the prior six months, reflecting the actions taken to reduce costs as well as the momentum gained in underlying revenue. |

|

· |

Underlying loss before tax was £48.0 million, a reduction of 22% from the £61.3 million loss in H2 2021 and a reduction of 56% from the £110.0 million loss in H1 2021, highlighting the trajectory towards sustainable profitability. |

|

· |

Statutory loss before tax of £60.2 million in H1 2022 (H2 2021: loss of £106.2 million) includes the capital neutral impairment of intangible assets (£8.2 million) and remediation costs (£3.0 million). Remediation costs have sharply reduced as we continue to close out legacy issues. For example, we concluded the matter with US Office of Foreign Assets Control (OFAC) in relation to Cuba and Iran without fine or penalty. |

|

· |

Statutory loss after tax of £61.7 million in H1 2022 (H2 2021: loss of £107.1 million) after a £1.5 million corporation tax charge. |

Capital, Funding and Liquidity

|

· |

Strong liquidity and funding position maintained, the Bank’s Liquidity Coverage Ratio (LCR) remains elevated at 257% as of 30 June 2022 (31 December 2021: 281%). Whilst NIM dilutive, this excess liquidly is earnings neutral and provides flexibility and optionality. |

|

· |

Common Equity Tier 1 (CET1) ratio of 10.6% as at 30 June 2022 (31 December 2021: 12.6%) compares to a minimum CET1 requirement of 4.8%7 and minimum Tier 1 requirement of 6.4%7. |

|

· |

Total capital ratio of 13.8% as at 30 June 2022 (31 December 2021: 15.9%) compares to a minimum requirement of 8.5%7. |

|

· |

MREL ratio of 18.3% as at 30 June 2022 (31 December 2021: 20.5%) compares to a minimum requirement of 17.0%7. |

|

· |

The PRA reduced the Bank’s Pillar 2A capital requirement from 1.11% to 0.50% effective as of 27 June 2022. The Resolution Directorate of the Bank of England also agreed that the Bank’s binding MREL applicable from 27 June 2022 shall be equal to the lower of: i) 18% of the Bank’s RWAs; or ii) Two times the sum of the Bank’s Pillar 1 and Pillar 2A Therefore the Bank’s minimum MREL requirement7 has been reduced to 17.0%. |

|

· |

Total RWA as at 30 June 2022 was £7,702 million (31 December 2021: £7,454 million). The increase reflects the mix improvement towards higher yielding assets. The result is a loan risk weight density of 49% as at 30 June 2022 (31 December 2021: 48%). |

|

· |

Regulatory leverage ratio8 was 4.3%. |

|

7. Minimum capital requirement excluding buffers. 8. The PRA Policy Statement 21/21 took affect from 1 January 2022 which required the exclusion of certain central bank claims from the total exposure measure. Had the central bank exposures been included the Leverage Ratio would have been 3.8%. |

|

Outlook and Guidance

|

· |

The path to profitability is supported by the continued mix improvements and balance sheet growth alongside ongoing cost control and benefits from rate rises. Profitability: Monthly breakeven is expected during Q1 2023, assuming no material deterioration in the macroeconomic environment. |

|

· |

Momentum continues towards profitability as margins widen:  |

|

· |

Guidance provided in February 2021 for 2022 full year, as set out below, is re-affirmed although we remain cognisant of the potential for unexpected adverse macroeconomic developments, which may impact our ability to deliver on guidance. Loan growth expectations are now higher for the year as the Bank continues to optimise balance sheet growth within capital constraints. Balance sheet: Higher growth than 2021 (2021: 2%) with continued focus on mix improvement. Margin: A 1.56% FY21 exit NIM holds us in good stead for 2022 with continued focus on lending mix and improved yields as a result of the base rate rises, potentially tempered by higher cost of deposits. Fees: Transaction-driven revenue streams influenced by the pace of recovery. Costs: Low single digit % reduction in total underlying operating expenses. Non-underlying items are expected to be less than 20% of 2021 (2021: £73.8 million) as remediation costs fall away. Capital: As previously stated we are comfortable operating in buffers and remain above regulatory minima (currently 17.0% for MREL). The Bank’s AIRB application is progressing. Alternative capital actions remain available. |

A presentation for investors and analysts will be held at 8.30AM (UK time) on 28 July 2022. The presentation will be webcast on:

https://webcast.openbriefing.com/metrobank22/

For those wishing to dial-in:

From the UK dial: 0800 640 6441

From the US dial: +1 855 9796 654

Access code: 828004

Metro Bank PLC

Summary Balance Sheet and Profit & Loss Account

(Unaudited)

For more information, please contact:

Metro Bank PLC Investor Relations

Jo Roberts

+44 (0) 20 3402 8900

Metro Bank PLC Media Relations

Tina Coates / Mona Patel

+44 (0) 7811 246016 / +44 (0) 7815 506845

Teneo

Charles Armitstead / Haya Herbert Burns

+44 (0) 7703 330269 / +44 (0) 7342 031051

ENDS

About Metro Bank

Metro Bank services 2.6 million customer accounts and is celebrated for its exceptional customer experience. It is the highest rated high street bank for overall service quality and best bank for service in-store for personal and business customers, in the Competition and Market Authority’s Service Quality Survey in February 2022. This year it has been awarded “Best Mortgage Provider of the Year” in 2022 MoneyAge Mortgage Awards, “Best Business Credit Card” in 2022 Moneynet Personal Finance Awards and “Best Current Account for Overseas Use” by Forbes 2022. It was “Banking Brand of The Year” at the Moneynet Personal Finance Awards 2021 and received the Gold Award in the Armed Forces Covenant’s Employer Recognition Scheme 2021.

The community bank offers retail, business, commercial and private banking services, and prides itself on giving customers the choice to bank however, whenever and wherever they choose, and supporting the customers and communities it serves. Whether that’s through its network of 76 stores open seven days a week, 362 days a year; on the phone through its UK-based contact centres; or online through its internet banking or award-winning mobile app, the bank offers customers real choice.

Metro Bank PLC. Registered in England and Wales. Company number: 6419578. Registered office: One Southampton Row, London, WC1B 5HA. ‘Metrobank’ is the registered trademark of Metro Bank PLC.

It is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and Prudential Regulation Authority. Most relevant deposits are protected by the Financial Services Compensation Scheme. For further information about the Scheme refer to the FSCS website www.fscs.org.uk. All Metro Bank products are subject to status and approval.

Metro Bank PLC is an independent UK bank – it is not affiliated with any other bank or organisation (including the METRO newspaper or its publishers) anywhere in the world. Please refer to Metro Bank using the full name.