Third Quarter 2022 Trading Update

- Profitable on both an underlying and statutory basis for September, ahead of previous guidance

- September performance is encouraging given it is driven by margin improvement and cost discipline

- Active balance sheet management and prevailing interest rates supported exit NIM of 2.04%

- Expect NIM to improve through 2023 given evolving balance sheet composition, base rate increases and deposit pricing discipline

- The pace of NIM improvements will be impacted by capital constraints limiting lending growth

For the month of September the Bank recorded a profit on both an underlying and statutory basis, ahead of expectations, driven by assertive balance sheet action, strong NIM expansion to 2.04% and continued cost discipline.

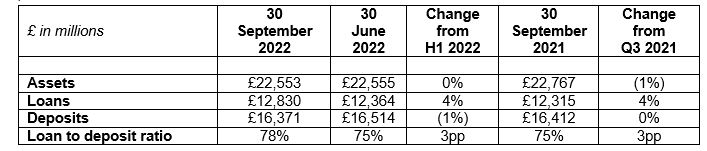

Q3 total deposits of £16,371 million were broadly flat reflecting ongoing close management of deposits. The Bank continues to attract low-cost high-quality deposits, evidenced by growth in the underlying deposit franchise (low-cost demand current and savings accounts) now 96% of the deposit base, offset by a targeted reduction in higher-cost fixed term deposits.

Q3 total net loans of £12,830 million increased 4% both QoQ and YoY, with a continued mix shift in line with strategy. Residential mortgages and consumer unsecured lending grew, partially offset by repayments of government-backed lending and reduction in Commercial real estate lending. The Bank is appropriately positioned, with a loan to deposit ratio of 78% and 55% of the loan portfolio being Residential mortgages. Over 90% of the Retail mortgage portfolio is fixed, with an average repricing duration of 2.1 years, and the average DTV of 56% remains stable. In aggregate only 5% of Retail mortgages now have a DTV of over 80%.

ECL Charge of £10 million in the quarter. There has been no deterioration in early warning indicators and no signs of stress or increased delinquency across the customer base. The Bank continues to monitor all of its portfolios closely and remains watchful of changes in economic conditions that may impact provisioning, such as material movements in unemployment from its current historically low point. Post model adjustments and overlays continue to be more than 24% of total provision stock.

Following a profitable month in September and positive underlying business momentum, going forward, the main driver of capital consumption is likely to be loan related RWA growth, which is currently being assertively managed to ensure the Bank continues to operate within buffers and remains above regulatory capital minima. Although mindful of the macro environment, minimum regulatory capital requirements are expected to be met without needing to take any market-dependent balance sheet action. The Bank will continue to review market-dependent options to manage regulatory capital and MREL and enhance its medium-term earnings potential, such as loan sales and securitisations as well as MREL qualifying debt issuance should market conditions be attractive. Management continues to engage with key stakeholders around the Tier 2 instrument. In all cases the goal is to create a more efficient balance sheet. Additionally, the Bank’s AIRB application continues to progress.

Daniel Frumkin, Chief Executive Officer at Metro Bank, said: “I am really pleased to see the business return to profit in September on both an underlying and statutory basis. This performance reflects our tight control of both costs and risk, close management of our deposit franchise and lending channels, and the supportive prevailing interest rate environment, all of which help build a balance sheet that delivers sufficient margin to cover costs. Whilst we remain watchful of economic conditions and continue to monitor our credit metrics closely, our book remains in good health. The underlying potential of our business is encouraging and, though the tight capital position currently constrains RWA growth, the business still seeks to grow margins with ongoing optimisation and discipline. We remain focused on generating a sustainable business supported by the commitment and engagement of our tremendous colleagues who continue to be there for our customers and communities.”

For more information, please contact:

Metro Bank PLC Investor Relations

Jo Roberts

+44 (0) 20 3402 8900

Metro Bank PLC Media Relations

Mona Patel

+44 (0) 7815 506845

Teneo

Charles Armitstead / Haya Herbert Burns

+44 (0)7703 330269 / +44 (0) 7342 031051