Metro Bank PLC has delivered a strong trading performance for 2016.

2016 Full Year Highlights

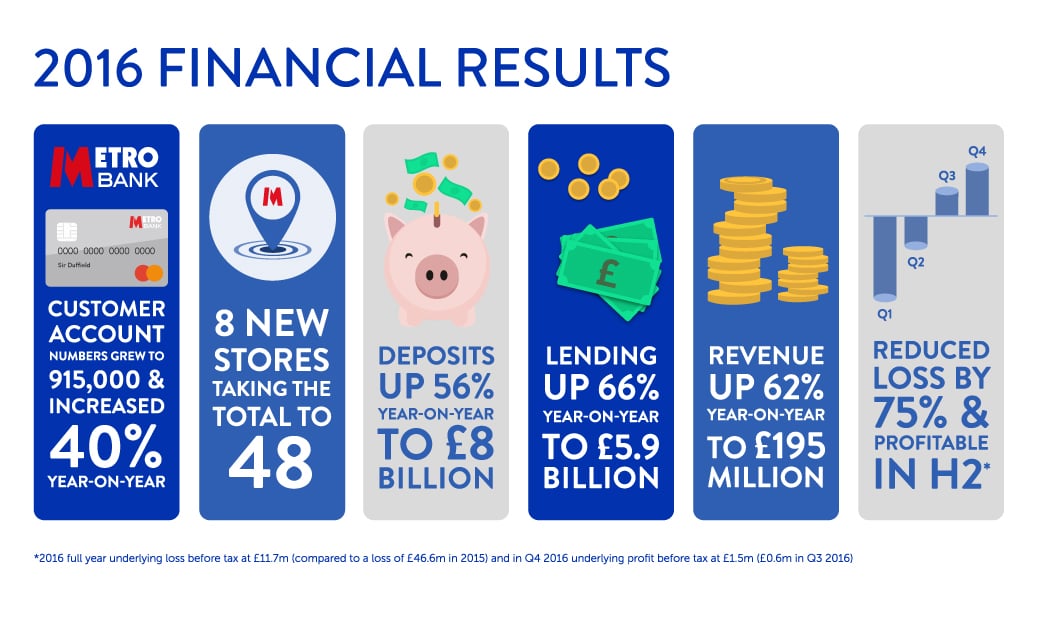

- Asset growth up 64% year-on-year to £10,057m ($12,370)

- Record deposit growth; up 56% year-on-year to £7,951m ($9,780m)

- Record lending growth; up 66% year-on-year to £5,865m ($7,214m)

- Loan to deposit ratio increased to 74%

- Revenue up 62% year-on-year to £195m

- Record 260,000 increase in customer accounts to a total of 915,000

- Strong Common Equity Tier 1 capital ratio at 18.1%

- Underlying loss before tax (1) at £11.7m (compared to a loss of £46.6m in 2015)

Q4 Highlights

- Deposits from customers up 9% quarter-on-quarter to £7,951m ($9,780m)

- Lending up 13% quarter-on-quarter to £5,865m ($7,214m)

- Revenue up 8% quarter-on-quarter to £57.6m

- Underlying profit before tax (2) at £1.5m (£0.6m in Q3 2016)

Note: all figures contained in this announcement are unaudited. All figures in US$ have been translated at a rate of $1.23 to the £.

| Quarter ending £ in millions | 31 Dec 2016 | 30 Sept 2016 | Change in Quarter | 31 Dec 2015 | Change in Year |

|---|---|---|---|---|---|

| Assets | £10,057 | £9,005 | 12% | £6,148 | 64% |

| Loans | £5,865 | £5,193 | 13% | £3,543 | 66% |

| Deposits | £7,951 | £7,297 | 9% | £5,108 | 56% |

| Loan to deposit ratio | 74% | 71% | 3 bps | 69% | 5 bps |

| Total Revenue | £57.6 | £53.4 | 8% | £34.3 | - |

| Underlying profit/(loss) before tax | £1.5 | £0.6 | 162% | (£12.5) | - |

| Underlying profit/(loss) after tax per share | £0.02p | £0.00p | - | (£0.17p) | - |

| Net interest margin | 2.03% | 1.95% | 8 bps | 2.01% | - |

(1) Underlying profit/ (loss) before tax for the year excludes listing and related costs and impairment of plant & equipment and intangible assets. Statutory loss before tax at £17.2m (compared to a loss of £56.8m in 2015)

(2) Underlying profit/ (loss) before tax for the quarter excludes listing and related costs, the FSCS levy and impairment of plant & equipment and intangible assets. Statutory profit before tax at £0.9m (compared to a profit of £0.02m in Q3 2016)

Craig Donaldson, Chief Executive Officer at Metro Bank said:

“It’s been another great quarter and I’m delighted with our full-year performance. We continue to show significant growth across lending, deposits and customer account numbers with continued integration of technology across all our channels, including stores, creating a compelling service experience for our retail and business customers.“

“The year saw continued major investment in technology, stores and colleague training – c. £100m in total – helping us to achieve a 62% full year increase in revenue and our second successive quarter of profitability. Our absolute focus on creating FANS through our model, culture and fanatical execution goes from strength-to-strength.”

Vernon Hill, Chairman and Founder at Metro Bank said:

“The response of the British public to Metro Bank has exceeded our expectations. Our goal is to create a legendary, emotional brand by creating FANS who join our brand, remain loyal and bring their friends. I’m very proud of the bank’s success over the past 12 months, and my thanks go to our colleagues, investors and FANS who are Metro Bank. I am confident that this is just the beginning, the best is yet to come.”

Financial Highlights for the Year and Quarter Ended 31 December 2016

- As of 31 December total assets were £10,057m, up from £9,005m at 30 September 2016 and £6,148m at 31 December 2015; representing year-on-year growth of 64% and 12% growth in the quarter.

- Record net deposit growth per store per month of £5.7m ($7.0m) in 2016 compared to £5.3m ($6.5m) in 2015 showing the strength of the network effect.

- Comparative store deposit growth (a measure of deposit growth using deposit numbers from stores that have been operating for more than a full year) is 51%.

- The loan to deposit ratio increased to 74% (30 September 2016: 71%; 31 December 2015: 69%).

- Delivered two consecutive quarters of profitability: underlying profit before tax of £1.5m in Q4 2016 (compared to £0.6m in Q3 2016 and a £3.4m loss in Q2 2016). Statutory profit after tax improved to £0.6m (compared to losses of £0.4m in Q3 2016 and £5.9m in Q2 2016).

- For the year ended 31 December 2016, underlying loss before tax improved by 75% to £11.7m (2015: £46.6m). Statutory loss before tax improved to £17.2m (compared to a loss of £56.8m in 2015).

- Cost of deposits in Q4 was 66bps, a reduction from 80bps in Q3. This reflects deposit re-pricing following the reduction in Base Rate in August and strong growth in current accounts.

- As of 31 December total deposits were £7,951m, up from £7,297m at 30 September 2016 and £5,108m at 31 December 2015; representing year-on-year growth of 56% and 9% in the quarter. Deposits for the fourth quarter grew £654m. Deposits from commercial customers represent 50% of 31 December 2016 total deposits (30 September 2016: 52%).

| 31 Dec 2016 £'m | 30 Sept 2016 £'m | 31 Dec 2015 £'m | % Change in Quarter | % Change in Year | |

|---|---|---|---|---|---|

| Demand: non-interest bearing | 2,282 | 2,019 | 1,380 | 13% | 65% |

| Demand: interest bearing | 3,513 | 3,167 | 2,123 | 11% | 65% |

| Fixed term | 2,156 | 2,111 | 1,605 | 2% | 34% |

| Deposits from customers | 7,951 | 7,297 | 5,108 | 9% | 56% |

| Deposits from customers includes: | |||||

| Deposits from retail customers | 3,945 | 3,537 | 2,411 | - | - |

| Deposits from corporate customers | 4,006 | 3,760 | 2,697 | - | - |

Total loans as of 31 December were £5,865m, up from £5,193m at 30 September 2016 and £3,543m at 31 December 2015; an increase of 66% year-on-year, and a 13% increase in the quarter. Loans to commercial customers represent 36% of total lending as of 31 December 2016 (30 September 2016: 35%).

| 31 Dec 2016 £'m | 30 Sept 2016 £'m | 31 Dec 2015 £'m | % Change in Quarter | % Change in Year | |

|---|---|---|---|---|---|

| Gross Loans and advances to customers | 5,872 | 5,202 | 3,549 | - | - |

| Less: allowance for impairment | (7) | (9) | (7) | - | - |

| Net Loans and advances to customers | 5,865 | 5,193 | 3,543 | 13% | 66% |

| Gross loans and advances to customers includes: | |||||

| Commercial loans | 2,087 | 1,824 | 1,273 | 14% | 64% |

| Residential mortgages | 3,604 | 3,202 | 2,157 | 13% | 67% |

| Consumer and other loans | 181 | 176 | 119 | 3% | 52% |

- Asset quality remains strong. Non-performing loans were 0.12% of the loan portfolio and the loan loss reserve as a percentage of non-performing loans was 103% at 31 December 2016. Cost of risk is 0.10% at 31 December 2016.

- Capital ratios remain robust and well above regulatory requirements. Common Equity Tier 1 Capital as a percentage of risk weighted assets is 18.1%. Regulatory Leverage ratio is 6.51%. A move towards the advanced risk based (AIRB) approach in the medium term as well as the potential for Tier 2 debt issuance present an opportunity to achieve greater capital efficiency.

Operational Highlights

- Customer acquisition goes from strength to strength. Customer accounts have increased from 848,000 on 30 September 2016 to 915,000 at 31 December 2016. This represents an increase of 40% year-on-year and an 8% increase in the quarter.

- We opened our 48th store in Basingstoke in Dec 2016, one of 8 opened this year, as well as improving our existing network by building a Private Banking suite above the Kings Road store and expanding our contact centre in Slough.

- Brand Recognition has increased to a record 84% in the London market (compared to 80% in July 2016); rising to 89% for those working full-time and 87% for the ABC1 demographic, according to a recent independent survey conducted by YouGov(3).

- Our continuous investment in technology and innovation has resulted in the delivery of an improved customer experience across channels. We launched a game changing new online commercial banking platform, a new public website, introduced ApplePay as well as being the first UK challenger bank to join the Faster Payments scheme.

- We’ve invested in our people, welcoming 500 new colleagues this year, developing the talent within the bank and building strength and depth in the Commercial and Business teams in particular.

Outlook

- We will strengthen our network with a further 10-12 new stores in 2017 as we continue to in-fill and expand our reach.

- We achieved quarter on quarter profitability in 2016 and expect to deliver a full year of profitability in 2017.

- We remain confident in our ability to achieve our 2020 guidance and have seen no significant change in customer behaviour since the European Referendum vote. Our disruptive model continues to go from strength to strength.

(3) Brand awareness figures are from YouGov Plc. Total sample size was 1,021 adults. Fieldwork was undertaken between 14-17 February 2017. The survey was carried out online. The figures have been weighted and are representative of all London adults (aged 18+).

2020 guidance:

- Number of stores: c.110

- Average net growth in deposits per store per month: c.£5.25m

- Loan to deposit ratio: c.80%

- Net interest margin + fees: c.3%

- Cost : Income ratio: c.60%

- Cost of risk: c.0.20%

- Leverage ratio: >4.0%

- Return on equity: c.18%

For more information, please contact:

Metro Bank PLC Press Office

Tina Coates

+44 (0) 7811 246 016

pressoffice@metrobank.plc.uk

Martin Pengelley/ Latika Shah

Tulchan Communications

+44(0)20 7353 4200

metrobank@tulchangroup.com